Canadian January CPI data due at 1330 GMT on Friday 23 February 2018

- CPI NSA m/m expected 0.5%, prior -0.4%

- CPI y/y expected 1.5%, prior 1.9%

Some bank previews (bolding mine), via

Bank of America / Merrill Lynch

- As Canada continues to grow above potential, we expect pressure on prices to increase.

- Risks are to the upside given the recent fiscal reform in the US, which should push US GDP growth closer to 3%(BofAML expectation is 2.7%). Stronger external demand means that risks to growth and0 to inflation are to the upside for Canada.

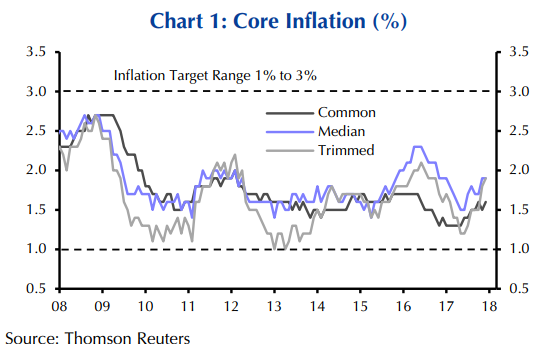

Capital Economics say "Core inflation to remain muted"

- Global bond markets have been shaken by the recent run of stronger wage and price inflation figures in the US. Although we have long expected that a rebound in core inflation south of the border would prompt the Fed to hike US interest rates more aggressively this year, we suspect that core inflation in Canada will remain slightly below the 2% mid-point of the Bank of Canada's target range.

- The Federal Reserve has come in for sustained criticism for undershooting its 2% target for the PCE deflator measure for almost a decade now. But, based on its new measures, the Bank of Canada is almost as culpable, even though the recession a decade ago was much more modest in Canada and was not complicated by a full-blown financial meltdown or housing crisis.

- January's consumer price data ... should show a modest rebound in gasoline prices from December. However, base effects caused by the big surge in energy prices a year ago mean that the annual headline inflation rate will still fall to 1.5%, from 1.9%. Nevertheless, the decline should be short lived, with an unwinding of those base effects pushing inflation back close to 2% in February.